A few years ago, the last time the flood maps were updated, I fought to have my house (the insured structure) removed from the AE flood zone. I did this with a Letter of Map Revision. The ‘test’ for this is if the “lowest adjacent grade” (the elevation of the dirt at the corners of you house) is high than the Base Flood Elevation (BFE) shown on the adopted FIRM then you qualify. Mine is and so I went back to qualifying for a “Preferred Risk” policy.

Now, with Risk Rating 2.0 being implemented my first renewal led to a premium of $687. I looked at the math and I could not see where the Community Rating System (CRS) discount was applied so I reached out to my insurance agent who looked into it and sent me this response: “In addition, I was advised that community 120217 has a 25% credit and that the total $687 premium is with that community credit, however, when I asked 25% of what amount I was told that the NFIP does not provide their rating information currently and that they can only verify the discount for the community number.” Sounded like hocus pocus, trust me it’s in there BS to me but I moved on.

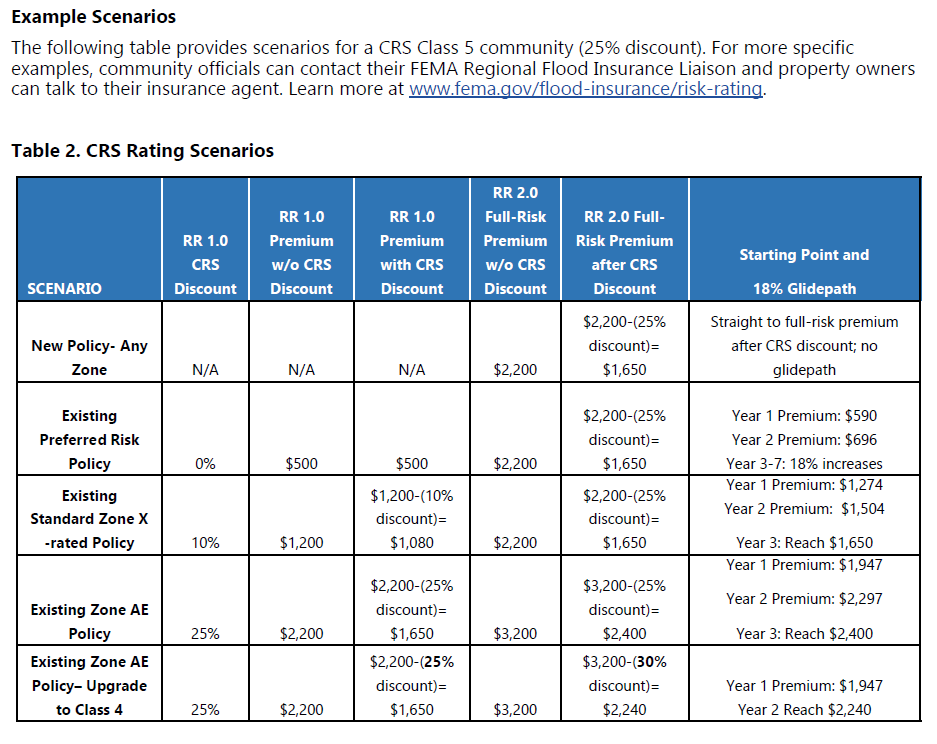

I was at a meeting the other day at the county and an insurance agent sent me: “Explaining the CRS discount in Risk Rating 2.0“. This has a great graphic in it to explain how the CRS applies to policy premiums under the new system. This table assumes a CRS Class 5 rating of the Community and thus a 25% discount applied. Basically, for most folks take the Annual Increase Cap amount shown on your policy renewal and multiply by 1.18.

This is a list of CRS rating for communities for April 2022.

Palm Beach County Properties enjoy a CRS of 5 (25% discount).

Village of North Palm Beach Properties enjoy a CRS of 5 (25% discount).

Juno Beach Properties enjoy a CRS of 5 (25% discount).

Jupiter Properties enjoy a CRS of 5 (25% discount).

Palm Beach Gardens Properties have a CRS of 10 (0% discount). YUP! No Discount.

Now, with Risk Rating 2.0, each policy is indivually rated and the mere fact that a property is in (or not in) a flood zone does NOT affect the premium.