How will the new high rise inspection law affect real estate?

By this time everyone knows about the tragic collapse of the Surfside Tower. In response to that collapse the state of Florida has several new laws meant to avoid this from happening in the future. How will these new laws affect real estate?

First is the new inspection requirements for any building which is 3 stories, or taller. The first deadline for these is coming up on 1 Jan 2023. By this date all condominium, co-op and apartment buildings are now required to file identifying information with the state’s Division of Florida Condominium, Timeshares and Mobile Homes.

After the state has all these buildings registered then we move to the next timeline.

- The law requires that a condominium or cooperative must have a “milestone inspection” performed for each building that is 3 stories or more by December 31st of the year in which the building reaches 30 years of age, and again every 10 years thereafter.

- If the building is located within 3 miles of a coastline, the inspection must be performed by December 31 of the year in which the building reaches 25 years of age, and every 10 years thereafter.

- If a building

107 Colony E Way Jupiter, FL 33458

107 Colony E Way Jupiter, FL 33458 in The Colony at Maplewood

High ceilings, granite countertops in the kitchen, a private backyard with screened patio, resort-like community swimming pool and spacious 2 car garage make this Key West style house an ideal place to call home. The Colony is an original 33 unit development built in 1989 by Concord Jupiter Development, Inc. a Casto company. Nestled in the heart of Jupiter with top-rated Schools, Shopping, Parks and Beaches all only a short drive away make this an ideal location to live. Residents also enjoy access to Maplewood Park and boat ramp on Jones Creek perfect for small vessels, paddle boarding and kayaks.

460 Ocean Ridge Way, Juno Beach, FL 33408

460 Ocean Ridge Way, Juno Beach, FL 33408 in Ocean Ridge

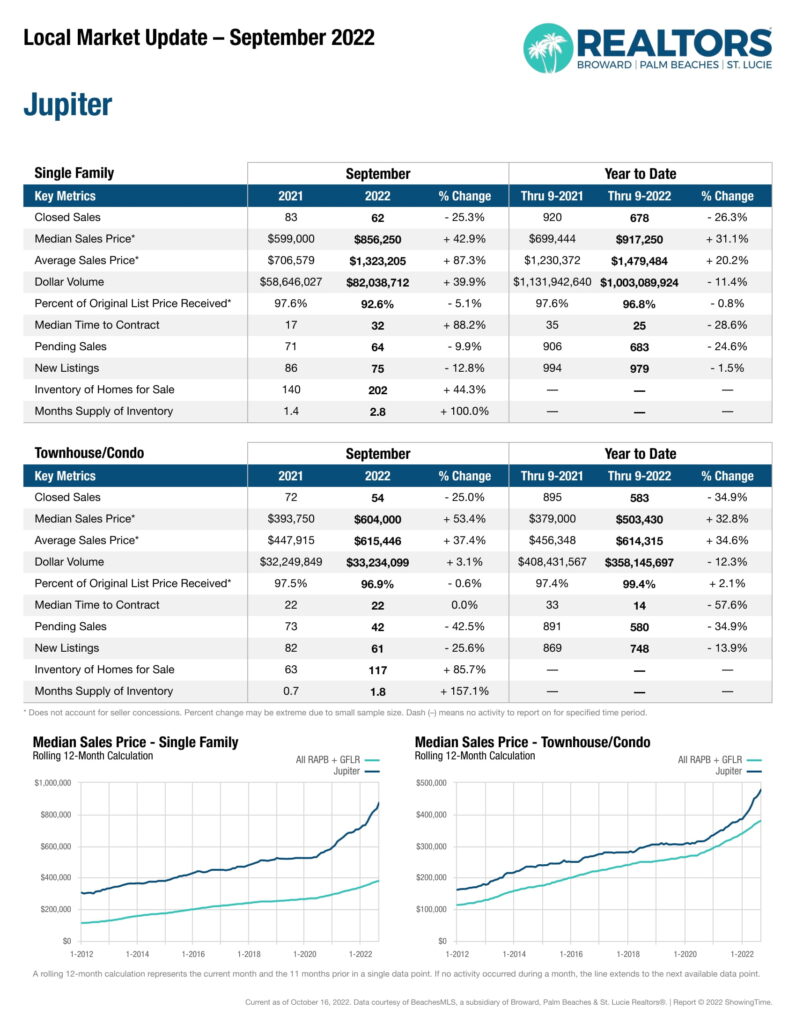

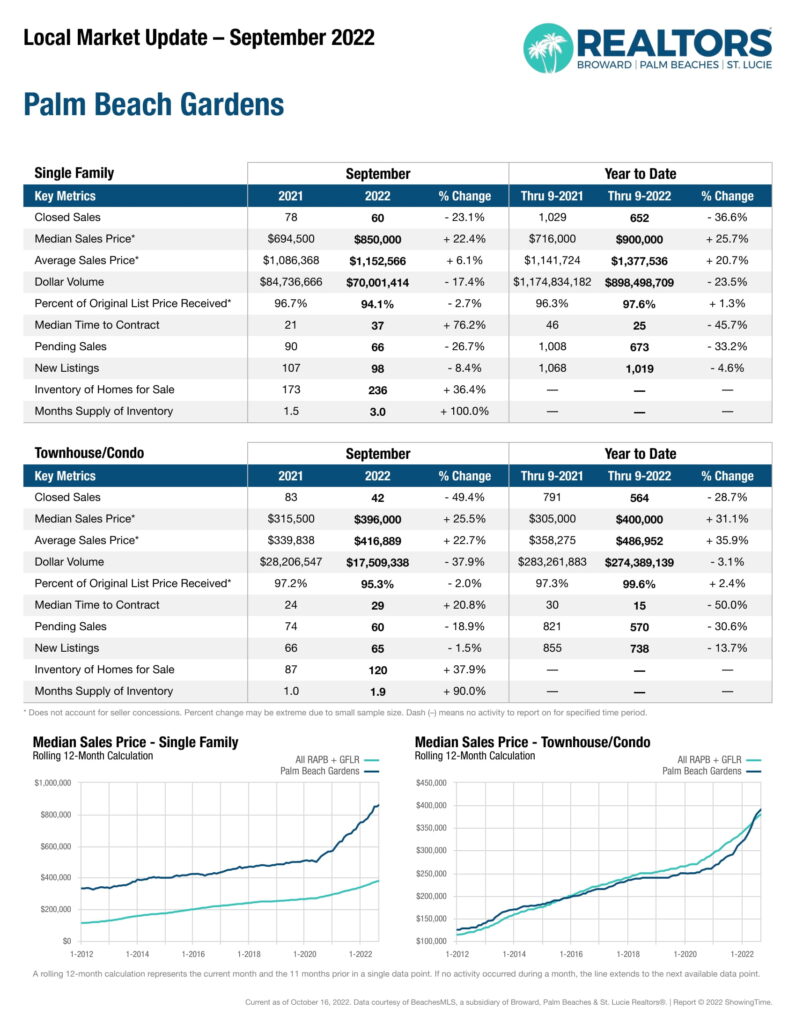

Housing Sales Stats for Jupiter and Palm Beach Gardens Florida for September 2022

The housing sales number were released a day ago and the local data for Jupiter and Palm beach Gardens reflects the county and the state sales numbers. The number of closed sales is off by about 30% and the months supply of inventory has doubled from a year ago. BUT, if we look at the numbers from last month we can see that this is leveling off at a bout a 3 month supply which historically for this area is a good Buyer-Seller balanced market.

504 E Tall Oaks Drive, Palm Beach Gardens, FL 33410

504 E Tall Oaks Drive, Palm Beach Gardens, FL 33410 is located in the Oaks East community.

Rarely available this waterfront DiVosta built home with over 2000 sq ft of living space is the largest floor plan in the community and includes an extended living area. All ceilings between 10 feet and 12 feet. 3 bed plus den/office, 2 bath and street facing 2 car garage afford comfortable living. Newer kitchen and second bath with comfort tub and separate shower in Primary bedroom en-suite bath. Roof 2016. Newly painted inside and out with pavers on patio at waterside and enlarged “green area’ for views and comfortable relaxing in your private sanctuary. 4 point and windmit inspection reports available. Poly plumbing replaced 2022. 5 minutes to Gardens Medical, Shopping and dining, 10 minutes to beaches, 20 minutes to PBIA.

- « Previous Page

- 1

- …

- 51

- 52

- 53

- 54

- 55

- …

- 159

- Next Page »