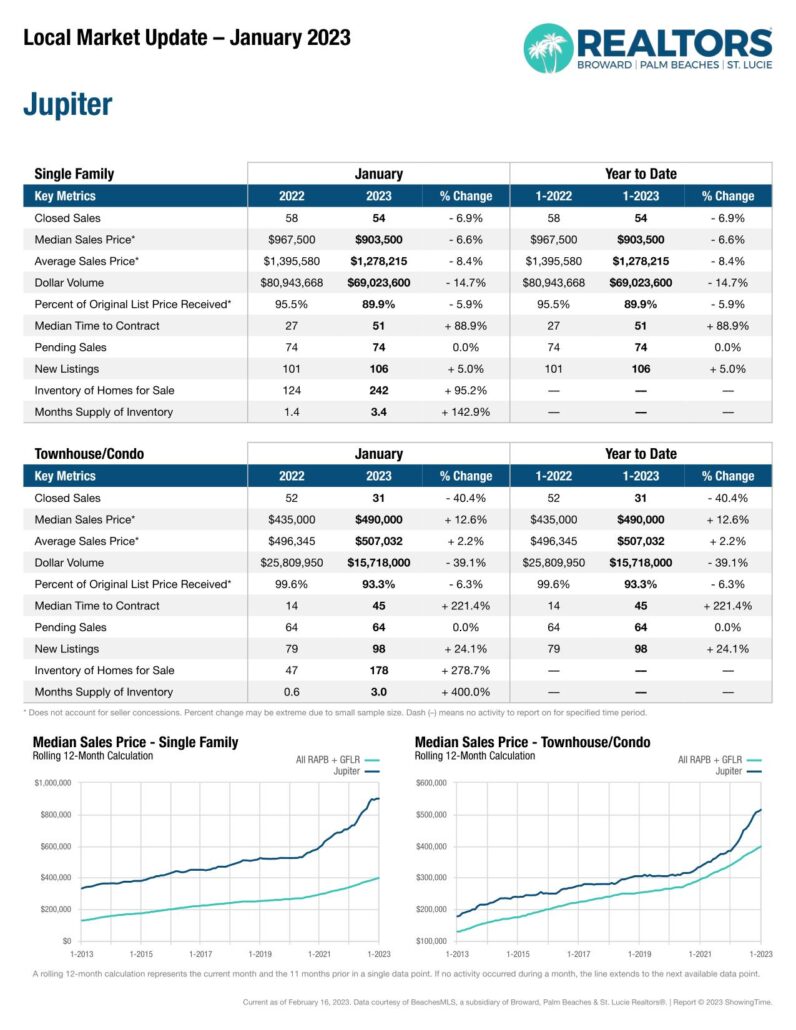

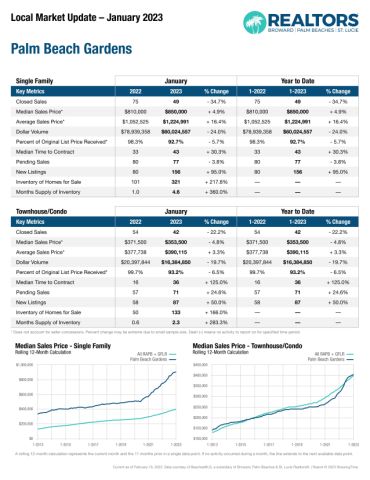

The Realtors Association of the Palm Beaches just released the January housing sales numbers and the numbers, as compiled, do not show the complete picture, IMO. I say this as they are comparing Jan 2022 with Jan of 2023 and we are in a very different market. The one stat that is interesting is the current Months Supply of Inventory. In my experiance, for this area, a 3.X months supply of inventory is a ‘balanced market’ and we see this is the case for all EXCEPT single family homes in Palm Beach Gardens.